For much of the last decade, the $80 to $150 budget phone tier was the device that brought hundreds of millions of Africans online. It was affordable enough to be aspirational, capable enough to run mobile banking apps, stream video, and access social platforms, and available enough to reach markets that global brands had long overlooked. According to new data from global market intelligence firm Omdia, that price band is now under severe structural threat, and the consequences for digital adoption across the continent could be significant.

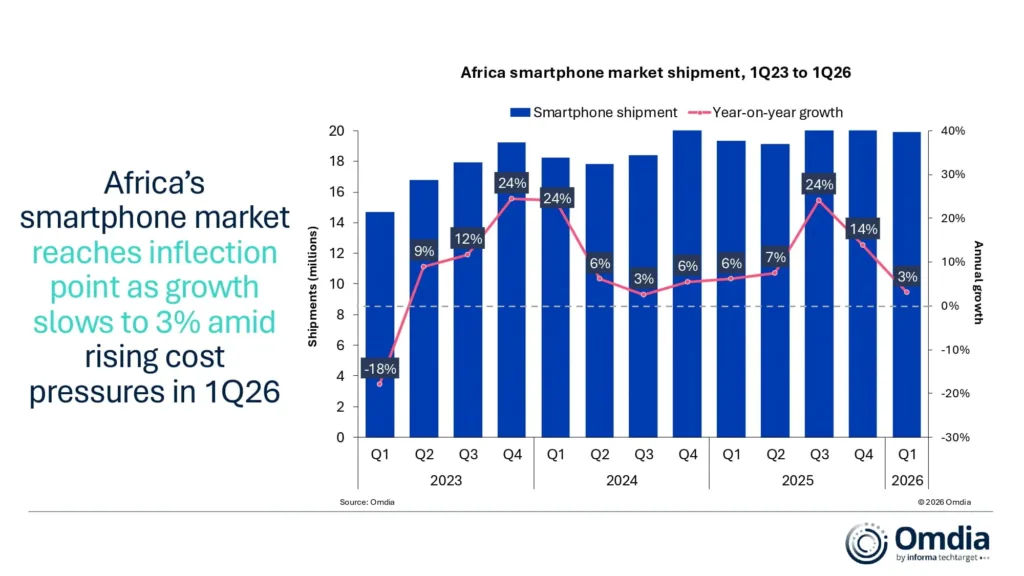

Omdia’s Q1 2026 African smartphone shipment report, recorded total continental shipments of 19.9 million units during the first quarter of the year, a modest 3% year-on-year increase compared to Q1 2025. On the surface, that headline figure looks stable. Dig into the geography and the vendor breakdown, however, and a far more uneven picture emerges.

A continent pulling in two directions

The 3% growth figure masks a sharp divergence between Africa’s regional markets. South Africa led continental performance with a 17% year-on-year increase, driven by robust device replacement cycles and consumers trading up to higher-specification handsets. The average selling price (ASP) of a smartphone in South Africa rose 4% to $369, anchored by Samsung’s premium ecosystem and a significant distribution push by HONOR into the upper mid-range segment.

Nigeria recorded 8% year-on-year growth, with volume expansion concentrated heavily in the $200 to $299 price tier. With persistent inflation and rising mobile data costs, Nigerian consumers demonstrated a clear willingness to stretch budgets in order to access reliable 4G and 5G connectivity.

Morocco also recorded positive momentum, with a 6% year-on-year increase following a reduction in import duties from 17.5% to 2.5%, a policy shift that improved both retail momentum and device affordability in the market.

Not every market shared that momentum. Algeria recorded the continent’s steepest decline, down 28% year-on-year, driven by a combination of strict government import regulations, acute foreign exchange shortages, and delays in establishing localised manufacturing operations to work around shipping restrictions.

Kenya fell 16%, with price-sensitive consumers opting to extend the life of existing handsets instead of upgrading at current retail prices. Egypt dropped 10%, pressured by weakened domestic consumer sentiment and supply chain disruptions tied to geopolitical tensions in the broader Middle East.

Buying a basic smartphone is about to cost a lot more

Beyond the geographic split, the more structurally important story in Omdia’s data is what is happening to pricing across the continent. The sub-$200 segment remained dominant in Q1 2026, accounting for 75% of total smartphone shipments. Africa’s market has always been built on volume at the entry tier, and that has not changed. What has changed is the economics underneath it.

Rising costs for memory, NAND storage, and semiconductor components are forcing device manufacturers to reprice their portfolios upward. The $300 to $499 mid-range segment expanded by 43% in Q1 2026, partly a product of this repricing and partly driven by the growing availability of device financing programmes. But for the vast majority of African consumers, a $300 to $499 device is not a realistic option.

The segment that built Africa’s smartphone adoption story over the last decade, the $80 to $150 tier, is the one Omdia flags as facing the most acute pressure. The firm projects a 28% contraction in the sub-$200 segment for the full year of 2026, with that specific price band bearing the brunt of compressed vendor margins. When the entry-level floor rises, the consumers closest to the bottom of the market are the first to be pushed out.

Omdia’s full-year projections suggest overall shipments could slip in subsequent quarters, a stark contrast to the growth momentum that characterised 2025.

Who is winning and who is struggling

Across the vendor market, the same pressures are playing out at different scales. TRANSSION retained its continental market leadership with a 47% share and 4% year-on-year growth, driven by high demand for budget models across its three sub-brands: Tecno, Infinix, and itel, each targeting distinct price points within the entry tier. The group’s deep last-mile distribution networks and localised manufacturing presence have given it a structural buffer that pure importers do not have.

HONOR recorded the highest growth of any major vendor, up 101% year-on-year, fueled by mobile operator partnerships in South Africa and the expansion of device financing options that brought higher-specification handsets within reach of a broader consumer base.

Samsung logged a marginal 1% decline but maintained its position in the $150 to $299 segment through the Galaxy A series and continued localised distribution operations in Egypt.

Xiaomi, whose portfolio on the continent spans its main line and POCO sub-brand, dropped 28% year-on-year as memory supply shortages cut deep into its entry-tier offering. OPPO fell 7%, affected by operational restructuring and weak performance in the Egyptian market.

The divergence between these trajectories is instructive. Omdia’s report notes explicitly that the vendors best positioned to survive the difficult second half of 2026 are those with established financing ecosystems, mobile operator partnerships, localised manufacturing setups, and extensive last-mile distribution networks.

What comes next

The 3% growth number deserves a closer look. A portion of it was driven not by fresh consumer demand, but by manufacturers importing extra stock early, getting ahead of rising component costs and weakening currencies before conditions worsened. That front-loading inflated Q1 figures in a way that will not repeat. The quarters that follow are starting from a thinner base than the opening data implies.

Africa’s young, mobile-first population continues to generate structural demand for digital access. That demand is not going away. But the devices that historically served as the on-ramp to that access are becoming harder to produce at prices that African consumers can absorb. If the $80 to $150 tier contracts as sharply as Omdia projects, the next wave of first-time smartphone users will wait considerably longer than the industry had planned for. For a continent where mobile connectivity underpins everything from financial inclusion to education access, that delay carries consequences well beyond the device market itself.