BNPL platforms in Zambia number far fewer than shoppers assume, and knowing that upfront saves a lot of wasted comparing. Only a small number of fintech options are verified and actively regulated by the country’s financial authorities for consumer installment payments, and just one of them is a dedicated retail checkout service in the way BNPL usually means elsewhere. This guide breaks down the actual state of BNPL in Zambia, who is actively offering it, and where traditional financing still fills the gap.

Quick Links

Why Zambia’s BNPL Market Is Still So Small

Buy now pay later has grown fast in countries with mature card payment systems, but Zambia’s payment habits run differently. Mobile money through Airtel Money and MTN MoMo dominates everyday transactions, and most digital lending in the country grew out of microfinance instead of retail checkout technology. That history explains why so few companies here operate true point of sale installment plans. Most of what gets marketed as BNPL locally is closer to a short term cash loan or a bill payment plan than the split pay checkout experience shoppers get used to on international platforms.

Regulation adds another layer. The Bank of Zambia oversees payment innovation through a Regulatory Sandbox, a framework that allows fintech companies to test new products under controlled, time bound conditions before they operate at full scale. The sandbox was set up specifically to let small-scale, live testing of payment innovations happen under the central bank’s supervision, instead of forcing every new product to meet full regulatory requirements from day one. Any platform claiming to offer BNPL in Zambia should be checked against this oversight, since it is the clearest signal of legitimacy in a market where new apps and services appear often.

BNPL Platforms in Zambia

1. Tupane Payments

Tupane is currently the most active, dedicated retail BNPL service in Zambia, and it operates officially inside the Bank of Zambia Regulatory Sandbox. Unlike app based competitors, Tupane runs entirely through USSD, dialing *290# to split a purchase into three interest free installments.

It relies on Airtel Money and MTN MoMo for both funding and repayment, which fits how most Zambians already handle digital transactions. Since it needs no smartphone app and no bank account, it is built for reach over convenience alone, and it is the closest thing the country has to a pure BNPL checkout product right now.

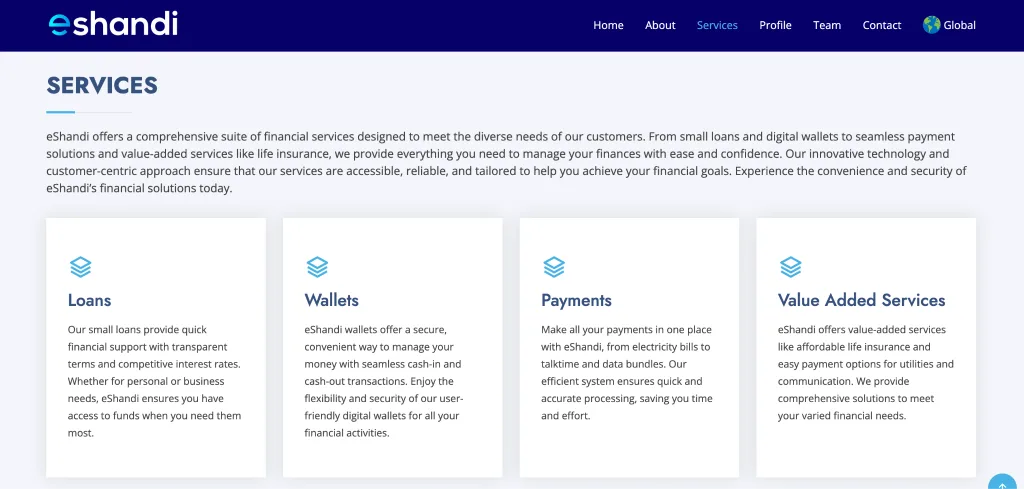

2. eShandi (formerly PremierCredit)

eShandi is fully licensed and regulated by the Bank of Zambia, and it offers structured smartphone financing and small personal loans through partnerships with telecom operators. Users apply through the eShandi portal or by dialing *559#. This is not a checkout style BNPL product in the strict sense, it functions more like a regulated microloan disbursed directly to a mobile money account, but it fills a similar need for buyers who want to spread the cost of a phone or a large purchase over time without going through a traditional bank.

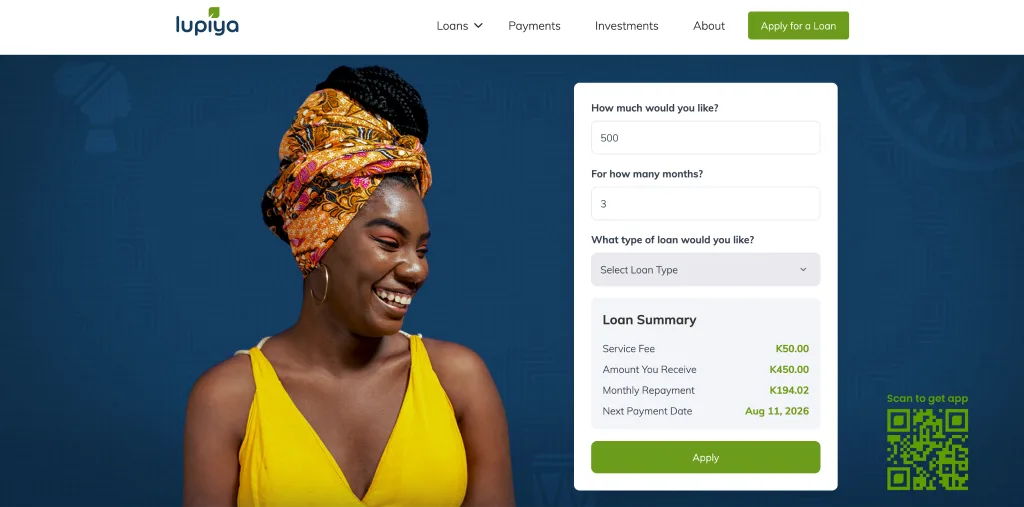

3. Lupiya

Lupiya is a prominent digital microfinance platform regulated by the Bank of Zambia, focusing primarily on instant personal cash advances, small business financing, and agricultural loans. Beyond their core credit lending services, the platform provides a digital wallet system that lets users transfer funds, handle peer-to-peer payments, and instantly settle standard utility bills like airtime, data, electricity, water, and pay TV.

Lupiya functions directly as a cash lender and a digital payment provider. It is not an integrated point-of-sale retail checkout system. Individuals looking to split retail store purchases can use Lupiya’s direct cash loan products to fund their consumer spending.

Traditional Hire Purchase in Zambia

Outside these three fintech platforms, most installment based buying in Zambia still runs through long standing brick and mortar Hire Purchase arrangements with individual retail chains. These setups need physical identity verification and usually involve monthly payroll deductions arranged directly with an employer, a model that predates digital fintech by decades and still moves a large share of appliance and furniture sales in the country. It is slower and less flexible than a digital BNPL app, but it remains the most established route for large purchases, especially for salaried workers whose employers already have payroll deduction agreements in place with specific retailers.

Which BNPL Platform Should You Use?

The right choice depends on what you are buying and how you want to repay it. If you want a straightforward, interest free split payment on a retail purchase, Tupane is the closest match to what BNPL usually means, and its USSD access makes it usable on almost any phone. If you need financing for a smartphone or a slightly larger personal expense and prefer working through a regulated lender with an app and portal, eShandi is the better fit, though it should be understood as a loan product and not a checkout split.

Lupiya remains a valuable platform if you already use its instant utility bill payment tools. For major purchases like furniture or appliances through a physical retailer, traditional Hire Purchase backed by payroll deduction is still the most common and accessible path for many Zambians.

Zambia’s BNPL space is young, regulated closely, and highly localized compared to larger regional financial markets. For buyers who want certainty, sticking with a platform under active Bank of Zambia oversight is the safest way to shop with confidence in this market.